In Florida, there are numerous strategies associations can use to fund reserves, but the two primary methods for calculating annual reserve funding requirements are the component method (straight-line or restricted reserves) and the cash flow method (pooled reserves). Funding using the component method was legally required in Florida for decades, meaning reserves could be used only for their “authorized purpose” unless approved in advance by the association’s members. Since the administrative code was adjusted in 2002, many associations have adopted the cash flow method, or pooled reserves. So, what are the component and cash flow methods, why would an association choose cash flow, and how do they make the switch?

Component Funding Method

The component method uses separate reserve accounts for each major project, with annual funding calculated as the unfunded portion of the replacement cost divided by the number of years until replacement is likely. A simple way to approach reserve funding, this method provides clarity on how each dollar is allocated and spent.

However, this approach offers no flexibility to move money between accounts. If there is a surplus in one account due to a lower-than-expected project cost or another reason, that money cannot be reallocated to another project without the homeowners’ prior approval.

Similarly, if a deficit arises in one account due to a project occurring earlier or costing more than expected, money cannot be drawn from other accounts to cover the difference. Additionally, the component method does not allow for the inclusion of inflationary factors in reserve funding calculations, which can cause capital projections to become less accurate over time.

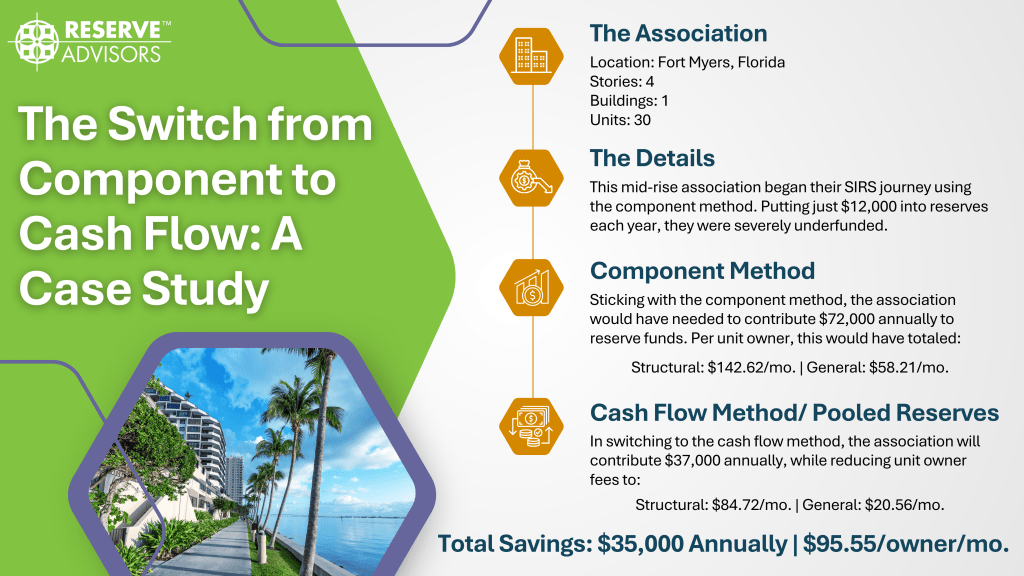

Cash Flow Funding Method

The cash flow method, commonly known as the pooled reserves method, is generally the recommendation of Reserve Advisors. This strategy involves putting all budgeted reserve contributions into one account – the pooled reserve. Because each dollar is not separately tracked, money can be spent on any project included in the reserve funding plan. Associations can still track reserve funding and spending on a line-item basis, but the funds themselves are contributed to a single account.

The required funding for a pooled reserve is based on the likely year-end balance of the reserve account in a high-expenditure year, also called a critical year, and on ensuring that funding in prior years is sufficient to keep the balance above a threshold of uncertainty determined by the reserve specialist and/or board. While determining this funding level is more complicated than the simple formula used for the component method, the benefits are significant.

First, associations can allocate all reserve assets to whatever project is necessary, even if that project exceeds the expected cost. Future projects can then be reprioritized until the reserve balance is high enough to fund them, and future funding can be adjusted based on the difference in the reserve account balances.

However, not all projects can be safely deferred, so this decision should be made in consultation with your reserve consultant. Second, this method allows you to incorporate inflation into cost projections, giving you a more accurate estimate of future project costs. The cash flow method also estimates the interest earned on reserve accounts and incorporates it into projections. Because of the flexibility offered by pooling reserves, most associations will see a significant reduction in required reserve funding levels.

Moving from Component to Cash Flow

There are two routes an association can take to transition from the component method to cash flow funding. First, the association can obtain a majority vote of the owning interests (a simple majority of owners – NOT a majority of a quorum) to reallocate existing reserve funds to a new “pooled” account.

The second method involves creating a new pooled account but not reallocating existing funds. With this approach, associations would contribute any new reserve funds to the pooled account and spend funds from the pre-existing component accounts until the component account balance reaches $0. While Reserve Advisors can provide industry recommendations on how to make this switch, the legality of each approach should be verified by an expert in Florida Condominium Law. We recommend consulting with professionals to determine the best course of action for your association.

The Bottom Line

Switching funding methods can be intimidating, and some boards may be hesitant to adopt the cash flow method. Because the component method locks down exactly where each dollar will go, they fear that switching to pooled reserves will allow subsequent boards to spend the money on unnecessary projects.

However, controls are in place to ensure reserves are used for their intended purpose, and boards have a fiduciary duty to act in their residents’ best interests. Over time, we have seen around 70% of Florida associations switch to pooled reserves, getting over their initial fear of adopting the cash flow method. It is incredibly rare that an association does not save money when making the switch, and that is usually due to unique circumstances with existing funds.

Overall, associations that have begun utilizing the cash flow method have seen decreased reserve contributions with no negative impact on capital replacement schedules.